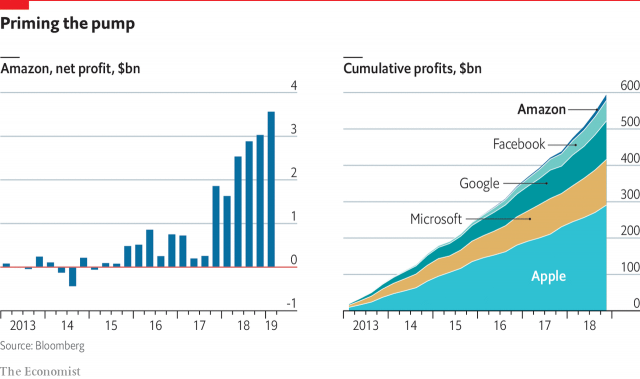

Amazon’s annual report indicates that their net margins showed a significant upward jump in their margins which have consistently hovered near 1% in the previous years.

The near-tripling of net-profit margins (also achieved at a much larger scale of revenues) arguably supports the hopes of enormous future margins — the rationale for high P/E values — sustained by the faith of some of the investors. My view is slightly different.

It is worth noting that despite significant upward jump in their profits, Amazon’s profits are a thin sliver compared to the big 4 tech companies, as the chart (below) from the Economist shows. This observation is not a criticism of the Amazon’s business per se. The thin margins shows the challenging nature of operating in Retail and focusing on scale.

So, in about 22 years after their IPO in 1997, has Amazon turned a corner, and will become similar to other tech firms with tremendous profit margins? My view is “No” and to support this assertion, I often cite the interview Jeff Bezos gave to Wired magazine in 2011:

“There are two ways to build a successful company. One is to work very, very hard to convince customers to pay high margins. The other is to work very, very hard to be able to afford to offer customers low margins. They both work. We’re firmly in the second camp…”

Amazon will continue to be a low-margin, large market-share firm that offers the best prices for the customers in every market segment. This implies that any profit margins will be continually reinvested into growth.

Usually in the core Operations class, my students debate whether such Amazon re-investments are a “choice” or “necessity”. My own view is that it doesn’t really matter. While it is hard to read intentions, it is easier to observe actions. Such low margins are results of the operational expenditures of being an innovative firm competing with firms with better profit margins. In the past, Amazon must have reinvested its profits based on discretionary spending or out of necessity.

In fact, few days after the annual report, I found another source of support to the point above, as Amazon announced their new one-day shipping policy for prime customers.

Getting Closer, Getting Faster and Getting More Expensive

This unilateral move to one-day shipping makes sense in the overall narrative of Amazon’s growth: The main story of retail growth for Amazon has been getting products closer and faster to customers, by building Fulfillment centers (and now stores) closer and closer to customers.

The cost-efficiency of one-day shipping is not clear. In fact, I have mentioned in the blog before, that last-mile deliveries are costly and inefficient. Given that there are 100 million customers on prime, unless there is a restriction on which products they will deliver in a day.

There must be some internal data at Amazon supporting one-day shipping speeds, but even for Amazon it must be expensive. However, the competitive advantage is that Amazon has additional $2 Billion (0.5% of their revenues) to reinvest into their delivery operations making it fast, even if it is inefficient. Firms following suit will only lose.

Walmart (another behemoth with cash on hand) has already hinted free 1-day deliveries.

There has never been a better time to be an e-commerce customer, and it has never been more challenging to be a small e-commerce business.