[Preamble: Readers — Posts had recently become infrequent and the blog had gone into a bit of hiatus, even though I have been engaged in teaching, a lot of personal journaling, writing, and research. The pandemic, is hopefully behind us, although one could not be sure about biological variants around the horizon. I am hoping this is a full-fledged return.]

Recently, I saw a news article from Nikkei Asia about Apple shifting the production of iPads from China to Vietnam. This appears to be mostly in response to the long covid-shutdown going on in Shanghai, which has disrupted Apple production a bit.

Nevertheless, there has been a slow but sure trend of manufacturing shifting out of China over the past few years, as a part of a secular trend. Sometimes glacial shifts don’t register until a massive sudden change precipitates all of a sudden. The shift in iPad manufacturing location is one such sudden event. It is a significant shift in capacity, given that Apple made more than 50m iPads in China, but the shift perhaps feels even more significant in our consciousness.

Wage Growth in China

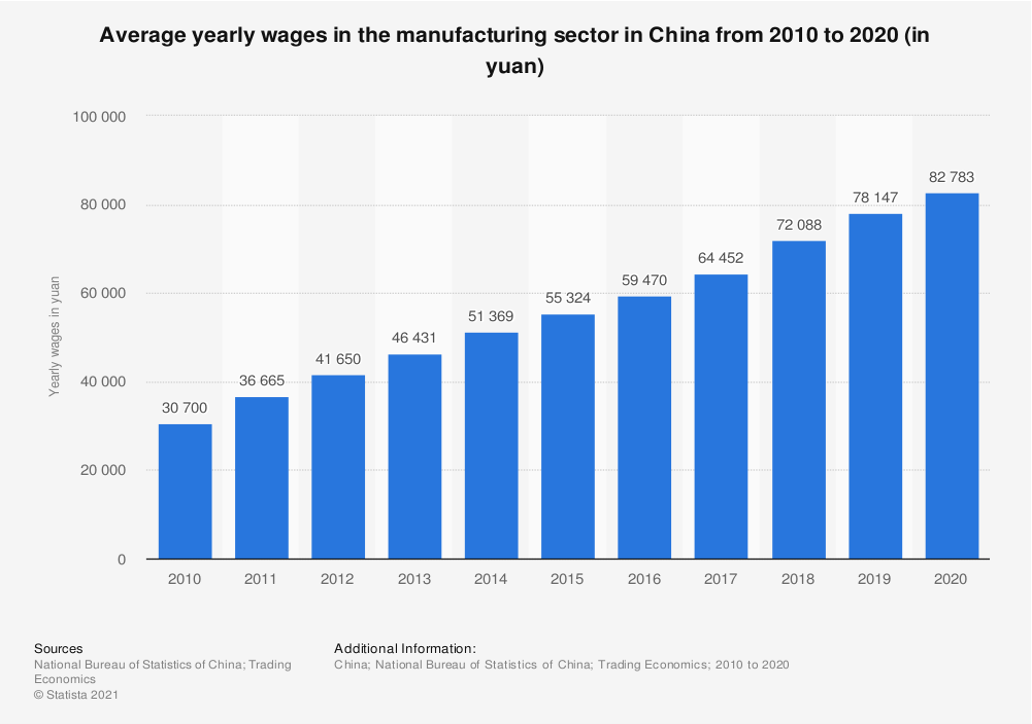

To understand Apple’s decision, it helps to examine how this capacity shift is necessitated by a trend over a long period. Here is data from the National Bureau of Statistics of China that I often show in my class. As the chart clearly shows, manufacturing wages have been growing steadily in China. To understand why this we have to look at a few demographic explanations (A post soon on this soon).

As the chart clearly shows, manufacturing wages have been growing steadily in China. To understand why this we have to look at a few demographic explanations (A post soon on this soon).

The effect of such growth is, however, very clear. Manufacturing wages now are substantial in China — nearly three times more than the wages a decade ago. Compare this growth to US manufacturing wages which have grown by at most 25% over the same period when wages in China tripled. Given the initial wage gap, a wage difference between US and China manufacturing will persist for a while. However, the wages in China have grown, fast enough to be higher than the manufacturing wages in adjoining in South East Asia.

Given the initial wage gap, a wage difference between US and China manufacturing will persist for a while. However, the wages in China have grown, fast enough to be higher than the manufacturing wages in adjoining in South East Asia.

This changes the manufacturing calculus of where to make products.

Scaled manufacturing has specific problems. Disruptions are costly. For sure, regardless of the observed wage trends, the lockdown situation in Shanghai was a proverbial “push” that forced Apple’s hands to shift capacity. Moving production to another location is complicated, because…

Supply Chains Are More Complicated than “mere” Manufacturing.

A firm cannot just shift its manufacturing plant and start production at scale. There is a ton of “know-how” to manufacturing at the scale that needs to be learned. Some of the learning, such as in Apparel manufacturing instance, happens at an accelerated pace and persists for a longer period, as there is a quite a bit of transfer learning that happens between products. Not so with electronic devices. Learning by doing proceeds slowly, and there is a significant process of learning for new products. A factory can’t just start manufacturing Macbooks because they have been making iPhones.

The second issue is almost supply chains are many tiered. In the case of electronic devices, one deals with large component manufacturers and suppliers, and even equipment manufacturers. By moving the manufacturing away to another location, a firm is very likely moving further from its suppliers. For iPad manufacturing, the observation is certainly true, that many of the suppliers are located in China.

What I mean by this is that even though the manufacturing is ostensibly shifting outside of China — the know-how is sticking within the supply chain. Firms like BYD that set up Apple’s assembly lines in China is also setting up their assembly in Vietnam.

One way to understand which products Apple has chosen to move to Vietnam depends on the maturity of the product, and whether the production process has scaled and matured.

For instance, even though Apple now produces a significant amount of Airpods in Vietnam, when it came to the development and production of the new generation Airpod 3, the production shifted to China. As MacRumors reported, one of the reasons this “reverse shift” happened was due to the need for product development talent.

One of the problems is said to be the need for so-called “new product introductions,” where companies and suppliers work together to develop and produce a completely new product. This has been especially difficult in Vietnam due to the lack of engineers able to work on AirPods 3 and other new devices.

Who holds the Inventory Risk?

Finally, it is worth noticing that just moving to a new production location does not eliminate disruption risk, as the suppliers and the production network continue to exist in China. So, how to overcome disruption risk? One way to do this is to bear risk through additional inventory readily available.

Buried in the article ($) on iPad capacity shift is Apple’s expectations from their suppliers.

To further guard against supply chain disruptions, Apple has also asked suppliers to build up additional supplies of components such as printed circuit boards and mechanical and electronics parts, especially those made in and around Shanghai, where COVID-related restrictions led to shortages and logistic delays. In addition, the company has asked suppliers to move quickly to secure supplies of some chips, especially power-related ones, for the upcoming iPhones.

In particular, Apple is asking suppliers outside of the lockdown-affected areas to help build up a couple of months’ worth of component supplies to ensure supply continuity over the next few months. The requests apply to all of Apple’s product lines — iPhones, iPads, AirPods and MacBooks — sources said.

To be sure, I think this is an onerous task. Apple has had a history of shifting inventory risk onto its suppliers. For example, I have heard that 3rd party suppliers have to hold products on consignment on their own books until they sell the products (or Apple charges a 100% buyback price on unsold goods).

By asking the suppliers to hold two months of inventory, Apple is shifting the inventory risk to the supplier. There is a possibility that the demand might collapse for the products. The domestic US demand (where most of the revenues for Apple devices come from) is tapering — due to concerns about inflation, wage stagnation, political uncertainty, and plain old, commoditization of the products. It is great for large firms that are able to shift their risk. If you are a smaller firm or a firm with barely any market power, it is harder to overcome the disruption risk by shifting it to supply chain partners to “share the pain”.